False Lessons From Japan

Puncturing Deflation Myths, Part 2

by Daniel R. Amerman, CFA

Overview

In Part 1 of this series on Puncturing Deflation Myths, we reviewed three logical fallacies, and showed why the US Great Depression didn’t prove the case for monetary deflation, but rather provided historical proof of how a sufficiently determined government could break monetary deflation at will, even in the midst of depression. In this Part II we will uncover three more logical fallacies as we:

1) Revisit our central question with regard to widespread theories about rapid and uncontrollable price deflation threatening symbolic currencies (“when has it ever happened in the real world?”) and review what actually happened with modern Japan;

2) Show the true peril experienced by Japan over the last 20 years, which is not monetary deflation but the much more deadly asset deflation;

3) Uncover the extraordinarily dangerous logical fallacy that results from confusing the two types of deflation, and show how this fallacy is currently leading millions of investors to mistakenly believe the value of their money is protected by bad economic times – when it has no protection at all; and

4) Briefly discuss why individual investors need to leave conventional financial wisdom behind and explore “outside of the box” solutions to these pressing issues.

Japan & “Where’s The Beef”?

As discussed in Part One, someone who had attended one of my inflation solutions workshops asked me to debate deflation theory with him. I said “fine” but with one condition: before I would debate theory, he needed to first provide a real word example of this problem actually having happened. Could he answer this simple, real world question:

Name an example of a modern, major nation where the domestic purchasing power (as measured by CPI) of its purely symbolic & independent currency uncontrollably grew in value at a rapid rate over a sustained period, despite the best efforts of the nation to stop this rapid deflation?

The two common answers to this question are the United States during the 1930s (addressed in Part I) and modern Japan. The Does Japan meet the conditions of this central question? Does it provide the real world “beef” for justifying theoretical monetary deflation fears?

Clearly Japan and the yen meet the criteria for modern, major, and symbolic. How about the domestic purchasing power of its currency uncontrollably growing at a rapid rate over a sustained period, despite the best efforts of the nation to stop this rapid deflation? After all, that is the very heart of the deflationist case for the US: that collapsing availability of credit will shrink both the volume and velocity of money, creating a rapid, powerful deflation that the government will be powerless to fight. Is that what happened in Japan? (Or anywhere else, ever, with a symbolic currency?)

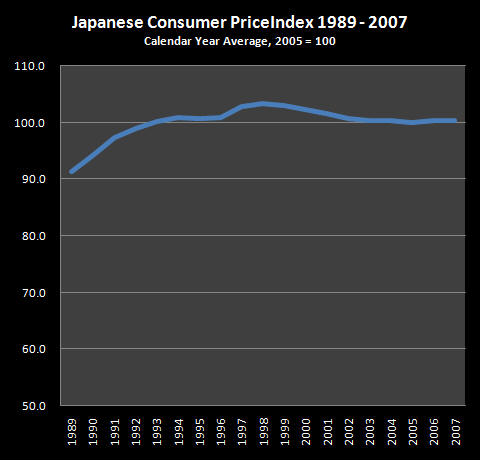

Maybe the best place to start is to see what actually happened to the domestic purchasing power of the yen during its time of economic “troubles”. The graph below tracks the average annual Japanese Consumer Price Index for the 19 year period from 1989 through 2007.

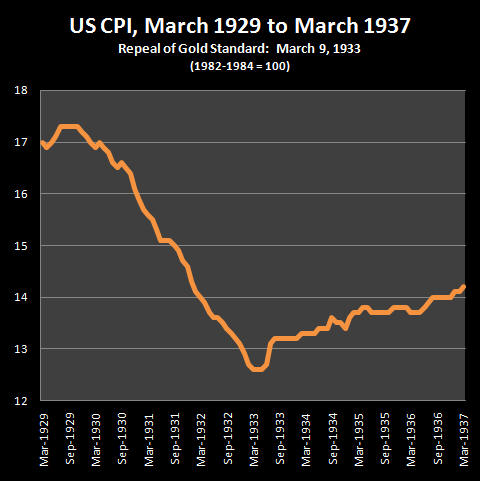

At first glance, that’s a pretty boring graph. Where is the drama and the action? Like that of the graph below from Part One of this article, which shows the US CPI during the Great Depression of the 1930s:

After looking at the US Consumer Price Index from 1929 to 1933 (or most global currencies during that period), the example of modern Japan looks quite tame in comparison. Where is the massive plunge? Where is that out of control monetary deflation that Japan was powerless to stop?

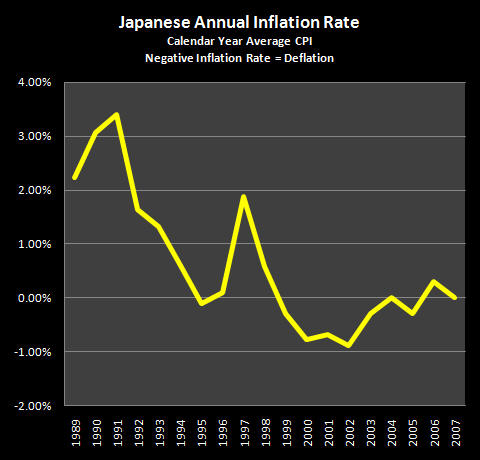

By historical standards, modern Japan clearly has not experienced major price deflation, not at all like the levels experienced by the US in the 1930s (and many nations at that time), or the bouts of severe deflation that hit repeatedly in the 1800s, when these nations were on a gold standard (as covered in Part I). Maybe this symbolic currency monetary deflation is there, but is hard to see? If it’s hard to see on a big graph with cumulative CPI, maybe we need to focus in and look at annual changes in the value of money:

When we look at the actual history of price (CPI) deflation in modern Japan, we can easily see:

1) At its worst – Japanese price deflation never reached even 1% per year, comparing average annual CPIs.

2) During the 19 years following the crash of the Nikkei, there where only 6 years of minimal deflation, and 13 years of inflation.

3) On a cumulative basis over these 19 years, Japan experienced price inflation, not price deflation. Indeed, the domestic purchasing power of the yen fell by 9% between 1989 and 2007, as shown in the first graph, “Japanese Consumer Price Index, 1989-2007”.

The Fourth Fallacy

When we put these three historical facts together, then we have our fourth common deflation fallacy (the first three fallacies are in Part One of this series). This fallacy is the widespread belief that Japan experienced powerful price deflation that it was unable to combat. In fact – the rate of price deflation never even reached one percent per year. This was an almost infinitesimal amount, and even a slight change in the calculation methodology could have led to no deflation at all. Also of importance is that arguably much or even all of Japan’s minor “deflation” resulted from increasing imports of cheaper goods from other nations, which has nothing to do with the collapsing credit of deflationist theories. Falling rents are the other main factor, but remove these imported goods, and the minor deflation disappears. The New York Times article from 2001, “Japanese Consumers Revel In Deflation's Silver Lining”, is an easy-to-read treatment of what real world modern deflation was like at the peak of Japan’s recent experience, that may be an eye-opener for many readers.

Article Link

This import driven (minor) price deflation, which was also key in slowing inflation in the US in the same time period (simply think China and Wal-Mart rather than esoteric macroeconomic theory), is a very different “animal” from collapsing credit availability – and therefore irrelevant to proving the argument. What also needs to be clearly understood is that this deflation is not independent of government policy, but is the direct result of government policy – the easing of import restrictions to increase the size of the overall economy. Japan could have almost instantly stopped its price deflation at will by simply changing import regulations.

Now granted, Japan has entered into international agreements to allow freer access to its domestic markets, as has the US, and there is the possibility that falling import prices from lower cost nations desperately trying to escape their own depressions could exert significant deflationary pressures in the future. But only if the governments let that happen. These free trade agreements came about because the developed nation’s citizens were assured economic prosperity in exchange for effectively allowing the destruction of many of their domestic industries. Replace promised prosperity with actual depression, let the political cycle go around a time or two, and import driven deflation is something that can and possibly will be stopped immediately in many or most nations. Because import driven deflation is not an unstoppable and independent economic force, but a creation of the political process.

When we return to our question asking for the single real world example of a symbolic currency rapidly and uncontrollably gaining in domestic purchasing power, despite the government’s best efforts to fight it – Japan clearly does not qualify.

So, once again - where is that real world example?

Do make sure you get an answer before betting your net worth on a theoretical argument about the inevitability of powerful and uncontrollable price deflation caused by a collapsing credit bubble, which governments will be powerless to fight.

Japan’s Catastrophic Experience With ASSET Deflation

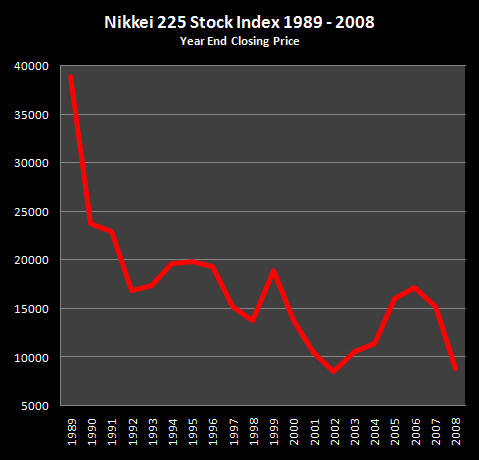

However, this is not to say that Japan hasn’t experienced powerful deflation over the last 20 years. Japan has indeed experienced major, even catastrophic deflation, that has savaged investor wealth and reduced the standards of living of many millions of Japanese as result – particularly the retirees. If you want to see a spectacular (and dismal) graph of Japanese deflation, here it is:

At the peak of the Japanese asset inflation bubble of the late 1980s, both the stock market and real estate market were hitting extraordinary highs, where the ability of companies to earn profits, and the ability of homeowners to make mortgage payments, had become almost irrelevant to stock and real estate prices. What mattered was price appreciation, and the more insane prices grew, the more investors piled in, to enjoy the fantastic paper profits that could be earned on the ride up.

That is, until the cycle turned, and the bubbles popped. The Nikkei hit 38,916 by the end of 1989 at the height of the exuberance – and then cold, hard reality started to hit. The Nikkei fell to 23,848 in the next year (down 39%), then 22,983 (down 41%), and then 16,924 by the end of 1992 (down 57% in 3 years). The full fall took 13 years, with the Nikkei 225 reaching 8,578 by the end of 2002, a 78% fall - something investors in other nations who are tempted to go bargain hunting today should keep in mind.

This is deflation of the very worst kind for investors in general and retirement investors in particular – but it isn’t price or monetary deflation. It is something far more dangerous, and that is asset deflation.

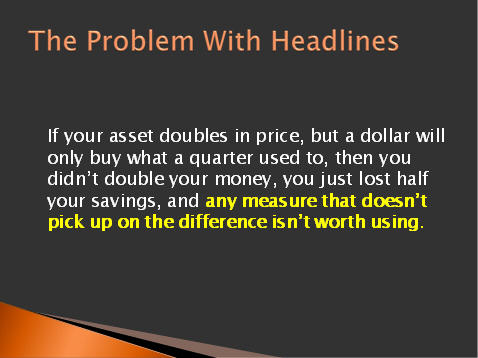

Price deflation is about falling prices for the goods and services you need to live and enjoy life. Because the prices for the things you need to buy are falling – your money buys more, meaning your real wealth is rising, all else being equal.

Asset deflation is about falling prices for the substantive assets that you have – such as your house and your investment portfolio. Because the prices for which you can sell your assets are falling, your assets buy less, meaning your real wealth is falling.

Both deflations are about falling prices – but that is where the similarity ends. The two deflations have opposite direct effects on your standard of living. The direct effect of price deflation is to raise your standard of living, and the direct effect of asset deflation (assuming you are selling rather than buying) is to lower your standard of living. So really we are talking about two quite different kinds of deflation, which may have the opposite effects on their standard of living for many people.

The Fifth Fallacy

Unfortunately, many financial commentators don’t understand the difference between the two fundamentally different kinds of deflation. This leads to our fifth logical fallacy in this series, and a return to the basic problem of comparing apples to oranges. In Part I, the apples and oranges fallacy was taking a history of price deflation based on gold-backed currencies, and saying it applies to purely symbolic currencies – despite the radically different long term histories of the two different types of currencies. Our fallacy in Part II is mixing up two quite different types of deflation. This lack of differentiation leads to the mistaken belief that Japan proves the case for modern price or monetary deflation. It doesn’t do anything of the sort – what Japan proves is the case for asset deflation – which is a quite different thing.

This confusion of terms is a deadly danger for individuals – and it really isn’t their fault. Economics professionals are of course well aware of the difference between the two types of deflation. When you look at academic texts such as “Deflation: Current and Historical Perspectives” by Burdekin and Siklos (Cambridge Press), it is about modern asset deflation, price deflation in the 1930s and before for gold-backed currencies, and theories about whether monetary deflation will return as a major danger. This same structure, which quite explicitly distinguishes between historical price deflation from the 1930s, actual modern asset deflation, and theoretical modern price deflation dangers, also applies to such works as the findings of the International Monetary Fund’s deflation task force, as reported in “Deflation: Determinants, Risks and Policy Options” (2003).

However, few people read such works directly. Instead, the information must pass through a filter, with the largest filter being the mainstream media. If the members of the media don’t understand the difference – their readers and viewers certainly won’t either. Indeed, in a world where it is exceedingly rare for the mainstream media to do something so basic and essential as report stock indexes and gold prices in inflation-adjusted terms, it should come as no surprise that the distinction between price deflation and asset deflation only rarely appears. Which leads most people, even very well read and highly intelligent people, to believe that there is only one kind of deflation – a mistake that can have devastating consequences for individuals and the value of their savings, as we will review in our sixth fallacy.

This differentiation between asset deflation and price deflation is very well understood by one particular group of professionals – and those are Japanese economists. Kazuo Ueda, Member of the Policy Board for the Bank of Japan, wrote an article specifically to address the popular confusion about what was happening in Japan, and the difference between general price and asset deflation. Here are two key quotes:

“There is much confusion in popular discussion of Japan's deflation and associated economic problems. This confusion tends to arise from a failure to distinguish between three related, but different phenomena: the stagnation of the real side of the economy, the deflation of general prices, and the deflation of asset prices. The deflation of general prices has certainly persisted since the mid- or late 1990s, depending on the price index one looks at. However, the extent of the price decline has been mild. The cumulative decline in the consumer price index (CPI) since its peak in 1998 has been no more than about 3%.”

“Declines in asset prices since the 1990s in Japan have been as large as they were during the Great Depression.”

The implications of this long fall in asset prices are extraordinary for investors in the United States and other nations. Indeed one could argue that the financial planning and pension management industry in the US was based upon a mutual agreement by everyone involved to close their eyes and pretend that Japan didn’t exist, with the full complicity of the government and academic community. To discuss what happened in Japan, and the vital implications for the US and other nations at this time, requires another full article, which will be part 3 of this series.

The Sixth Fallacy

Our sixth and most dangerous fallacy is the widespread belief that deflation protects us from inflation. This belief is false and indeed constitutes a deadly danger, because so many millions of people erroneously believe that falling asset prices protects the spending power of their money.

On the face of it – deflation protecting us from inflation looks so obvious, that it has to be true. If inflation and deflation are opposite and opposing forces – how could you possibly have both at the same time? Common sense therefore tells many people that as they read headlines about falling prices, one side benefit is that at least for now, they can stop worrying about inflation.

Unfortunately, this is a false sense of security that is based on the mistaken belief that there is only one kind of deflation, and that there is ample historical proof for this type of deflation. The common belief is that depressions generate monetary deflation, so inflationary dangers at least temporarily go away. Quite simply, this has never happened with a modern symbolic currency, not in a way that meets the requirements of the question posed earlier in this article. Collapsing credit availability and the resulting collapsing money supply leading to an unstoppable and rapidly rising value for a symbolic currency (price deflation) is a popular theory – but it has never happened in the real world. (At its core the theory is based on the naïve belief that a symbolic currency has some kind of inherent value aside from the rules which the government sets up, or that governments won’t change those rules when they have a strong incentive to do so. As discussed in my article “Why Inflation Will Trump Deflation”, the power of a government to reduce or destroy the value of its own symbolic currency is absolute.)

There is an extraordinary and well proven danger from catastrophic deflation when leaving bubbles behind and entering a depression or severe recession, but this deflationary danger isn’t monetary deflation – it is asset deflation. The core of the danger is that asset deflation doesn’t provide protection against monetary inflation. Instead, asset deflation and price inflation have a long history of occurring simultaneously in economically troubled nations, and working together to destroy wealth. Meaning that an investor who does not understand the difference between the two types of deflation, and therefore doesn’t maintain strong inflation defenses – is effectively “bare naked” as a result. For just because the value of your assets is plunging does not mean the value of your money is safe, not at all.

Basing their financial strategies off of this false assurance, many people are failing to take protective measures against inflation, even as they clearly see the Federal Reserve creating money without limit in tandem with the US government creating bailouts without limit.

When we look at collapsing credit and deflation – the relationship is very real and historically proven. Bidding up the prices of assets, or asset inflation, is often the result of cheap and easy credit financing the purchases of the assets. When the credit cycle tightens, then the lack of financing helps drive asset prices down, and a severe credit tightening like the current one can drastically drive prices down for a very long time. However, the combination of collapsing credit availability and the resulting collapsing asset prices leading to old-fashioned (gold standard type) major and unstoppable general price deflation – well, that is pure theory.

The Difference Between Theory & History

Let's re-examine the example of Japan. If we look at the value of the stock market, when everyone had purchased stocks in expectation of unending wealth, and that stock market is now down 80% on an after-inflation basis - where is the protection? Even in the face of an 80% asset deflation in real terms over a 20 year period, the Japanese yen is still worth less than when the period of deflation started. The massive asset deflation obviously did not protect the value of the currency.

It is also important to keep in mind that Japan is a poor example of economic “troubles” – it is a nation of a mere 127 million people, lacking most natural resources, which managed to maintain its position as the world’s second largest economic power for two decades of “troubles” (before accounting for Chinese currency manipulation anyway). It is this continuing strong economic performance (compared to the rest of the world) that accounts for Japan’s currency losing so little of its value.

For another real world example of how the value of the currency can fall simultaneously with the value of assets, let’s look at the world’s number one economic power: the United States. The US hit a period of economic turmoil between 1972 and 1982. The Dow stood at 929 in June of 1972, and by June of 1982 it had dropped to a nominal 812. It lost 13% of its value, and on the face of it, this is an example of moderate asset deflation. However, something else happened between 1972 and 1982: the dollar lost 57% of its value. When we adjust for inflation, the Dow Jones Industrial Average actually dropped from 929 to about 350 (in 1972 dollars), meaning it lost 62% of its value (exclusive of dividends).

That 62% reduction in value is powerful asset deflation – but here’s what that deflation and economic turmoil didn’t do – it didn’t protect the value of the dollar. A 62% drop in the purchasing power of assets did not protect the dollar from a 57% decline in its own domestic purchasing power. The ability of powerful deflation to protect the value of the currency failed spectacularly in practice.

Remember – the above is reality. A reality that has happened again and again in nations around the word that have gone through much worse economic stress than that experienced by the United States. Look at Iceland today. Or such well known examples as Argentina or Germany (or Zimbabwe) during their own bouts with high levels of inflation. In each case the purchasing power of assets was plunging simultaneously with the purchasing power of the currency. Which is exactly what you would expect for a nation in depression. The idea that going into a depression necessarily increases the value of that nation’s symbolic currency, when the currency is essentially backed by the economy, is a bit unusual when you think it through, and therefore the lack of historical precedents is not surprising.

The Six Fallacies

Let’s quickly review the six fallacies we have covered in Parts 1 & 2 of this article.

Fallacy One. The belief that a “dollar” is a “dollar” and that the deflationary history of gold standard currencies applies to symbolic currencies (an “apples to oranges” fallacy).

Fallacy Two. The belief that the US Great Depression proves the case for unstoppable monetary deflation during depressions, when it in fact proves that a sufficiently determined government can immediately break monetary deflation at will, even in the midst of depression.

Fallacy Three. The belief that inflation and deflation take wealth from all of us equally, when what they actually do is redistribute the wealth among us.

Fallacy Four. The widespread belief that Japan experienced powerful price deflation that the government was powerless to fight. It didn’t.

Fallacy Five. The fundamental mistake of thinking that “deflation” is “deflation”, which leads to confusing price deflation with asset deflation, and means missing the real lessons and dangers of what happened in Japan, which is the persistent asset deflation that has defeated all government interventions (another “apples to oranges” fallacy).

Fallacy Six. The dangerous belief that deflation protects you from inflation. More specifically, the vocabulary confusion that leads to the belief that asset deflation protects you from monetary inflation, or that the destruction of the value of your assets is somehow historically proven to protect the value of your money.

The six fallacies reviewed in this and the previous article come as quite a surprise to many people. We uncovered those fallacies – by improving our vision. Interesting though this is, better understanding what has happened in the past is not the primary reason for improving our inflation and deflation vision. More importantly, improving our vision allows us take personal actions for the future. As your vision improves further, you will come to understand that what all forms of inflation and deflation share is that they are redistributions of wealth among the individuals within a society. When we raise the degree of inflation and / or deflation, then we increase the opportunity for you have to have wealth redistributed to you by these fundamental economic forces.

In contrast to the six fallacies – let’s consider what clear vision can look like:

The above slide (from one of my courses) is an illustration of simultaneous monetary inflation and asset deflation. The one-two combination that annihilates retiree wealth and the value of long term savings for other investors.

Now if you believe that it is simply a matter of inflation versus deflation, and if you believe that all we're talking about is the destruction of wealth, then it is all too likely that your financial status in a situation like the above has been predetermined. You will be a victim of inflation and a victim of deflation. These forces acting in concert will take wealth away from you, and it may seem almost impossible to stop them if you are in the common situation of investing towards retirement and you have both substantial investment and monetary assets to protect. Because the double forces of monetary inflation and asset deflation will be working to simultaneously decrease the purchasing power for both your money and your investment assets.

There is hope, however. Indeed there are ways to take the situation introduced in the slide, where the value of your money drops by 75% and the value of your asset drops by 50% - and turn that into substantial profits on a tax-advantaged basis. Possibly some of the best returns of your life on an after-inflation and after-tax basis.

You need to get out of step with your generation, and have wealth redistributed to you even as your peer group is being devastated by this extraordinary destruction of wealth. For this to happen, you need to start with an essential and irreplaceable step: education. You need to gain the knowledge you will need to turn adversity into opportunity. This will mean looking inflation straight in the eye and saying: “Inflation, you are likely to play a big role in my personal future, and instead of ignoring you or thoughtlessly flailing away at you – I will study you and your ways. I will learn the deeply unfair ways in which you redistribute wealth, and the counterintuitive lessons about how some investors will be destroyed by inflation and repeatedly pay taxes for the privilege, even while other investors are claiming real wealth on a tax-free basis. I will learn to position myself so that you redistribute wealth to me, and the worse the financial devastation you wreak – the more my personal real net worth grows. I will examine the official blindness to inflation within government tax policy that creates the Inflation Tax, and instead of raging or despairing, I will understand that a blind opponent is a weak opponent, and I will take advantage of your blindness and use tax policy to multiply my real wealth.”

Remember – redistributions of wealth mean some people do worse – and other people do better. The higher the degree of inflation and/or the degree of deflation – the greater the redistribution of wealth. We are coming into a period of one of the greatest redistributions of wealth in our lifetimes, with extraordinary pressures building for both monetary inflation and continuing asset deflation (remember Japan’s fall in asset values lasted for 13 years). You have a choice to have wealth taken from you – or to find ways for wealth to be redistributed to you. To utilize that choice, you have to understand it fully, and all the nuances. Which means education. Otherwise, we’re just shooting in the dark.

(The article above was first published in March, 2009, during the early stages of the monetary deflation/inflation debate which followed the events of 2008.)