Bailout Lies Threaten Your Savings

Daniel R. Amerman, CFA, DanielAmerman.com

Overview

There is a headline that has been all over the media ever since September 2008: “Bank Bailout Will Soak Taxpayers.” As obviously true as this headline appears to be, it is in fact, dangerously misleading. Indeed, as we will cover in this article, the idea that taxes will pay for the bailout is ludicrous, an insult to both your intelligence – and your net worth.

Instead, the real source of the bailout monies will not be the taxes you pay, but the value of your savings. The value of your checking account, the value of your IRA or Keogh, and the value of all your investments are the true source of payment for Wall Street’s reckless mistakes. When we combine the bailout with the trouble the US was already in, the result could be a 95% reduction in value for all of our savings, retirement and otherwise, as we will illustrate step by step in this article.

There are things you can do. Actions you can take. Ways to defend the value of your savings, as we will discuss later. But before we talk about solutions, first we need to understand why taxes won’t pay for the bailout. Because it is only when we understand the real danger, that we can take effective action to protect ourselves.

Placing Things In Perspective

Let’s start by placing things in perspective. This financial crisis has not been happening in isolation. The United States government was already in an impossible financial situation before this crisis ever hit.

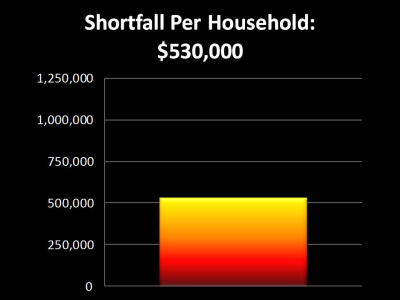

Looking at Social Security and Medicare, when we take a long term perspective, the projected excess of expenditures over taxes is at least $59 trillion according to a fairly well known and accepted study that appeared in USA Today. This isn't the total cost - it's the present value shortfall after taking out projected taxes at current levels.

Now, there are approximately 111,000,000 households in the United States. So if we take the total shortfall and we divide it by the number of households, we come up with a shortfall of over half a million dollars per household, and that number is reasonably well accepted these days.

Okay, you’ve probably seen that number before, or something like it. Now let’s very quickly do a few things you probably haven’t seen before.

Step One: Below Poverty Line Households

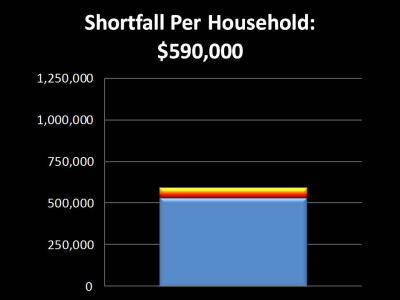

Our first step is to take the 11 million households that are below the poverty line and subtract them out. These households are already not really paying the federal government, they're getting paid by the federal government on a net basis, so we can't realistically expect them to come up with any of the money for Medicare or Social Security. When we take them out we're left with something very close to 100 million households.

Divide $59 trillion by 100 million households and our shares of the shortfall just jumped to $590,000 per household.

Step Two: Retired Households

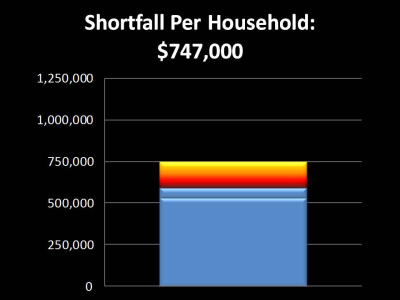

Step two is, do we expect retiree households to pay for their own retirement? Because when we say there's 100 million households, well, we’ve got quite a few retiree households already, and that number is going to be growing fast over the next 10 to 15 years as an average of 4 million baby boomers retire each year between 2010 and 2029. So if we look out over the decades ahead as the baby boom retires, and we adjust for the rapidly building number of retiree households who will be the beneficiaries of Social Security and Medicare – who will be receiving benefits rather than paying in – then we're left with an average of about 79 million households.

The 79 million households could be termed on average the number of households in which the primary source of income is someone who is below retirement age and actively working at a job that keeps them above the poverty line. In other words the people who can realistically make the economic contribution to pay significant taxes.

Divide 59 trillion by 79 million, and we all have to come up with $747,000 per household. We’ve now spent an additional $217,000 per household, compared to the USA Today number, but we’re not done yet.

Step 3: Pensions & Investments

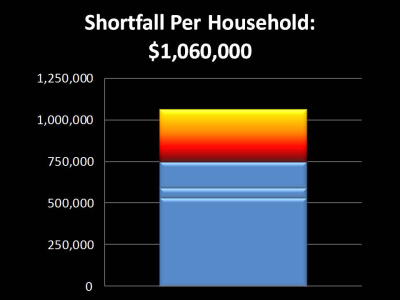

Step three is to say there's a lot more to the expenses of paying for retirement for the baby boom than just Social Security and Medicare. Legally binding promises for pensions have been made by all levels of state and local government as well as major corporations, which are going to require the cashing out of tremendous amounts of retirement investments. As well as the cashing out of those tens of millions of IRAs and Keogh accounts. Someone has to come up with money, or more accurately the real goods and sevices to do so.

So when we add in the cost of cashing out pensions and retirement accounts, we come up with a total figure per able to pay, non-retired household, including Social Security, Medicare, pensions and cashing out retirement investments, of $1,060,000 per household. (That was a quick derivation of Steps One through Three, much more thorough detail is available through my free mini-course.)

Bailout & Stimulus Cost

Now you might think spending a million dollars per US household in one short article would cover it all, but we’re still not done here, we’ve got a bailout and stimulus to pay for. How much is that going to cost?

The best answer is that no one knows for sure. Because the true cost of the bailout is so tightly interwoven with what is going on with the overall economy, as well as with the extremely complex and volatile market of over $400 trillion (still outstanding) in derivative securities contracts that have been entered into by banks around the world. Since the governments are guaranteeing the banks, that means they are guaranteeing the hundreds of trillions of dollars in derivatives, and we don't know what that’s going to end up costing.

Some people are saying no problem, we’ll get out of this for $1 or $2 trillion max, and by and large those are the same financial pundits who would have quite confidently assured you two years ago that a crisis like this was categorically impossible, something only a delusional paranoid would believe could happen.

Speaking not as a financial pundit, but as someone who actually structured derivative securities as an investment banker, who wrote a McGraw-Hill book on the subject in 1995, and who later forecast the steps in which the current crisis would unfold with uncommon precision - we’ve been lucky so far. We’re holding a tenuous line against a wider derivatives disaster that could make 2008 look like a cakewalk, and that line could crumble at any time.

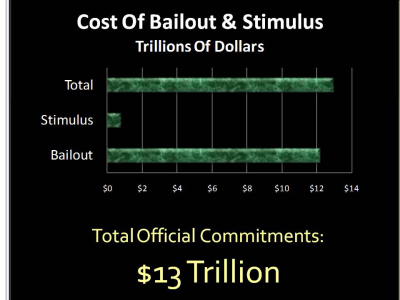

So the cost will likely be somewhere between $1 trillion and global financial collapse, but we do need a guess to work with, and maybe a place to start are the official actions of the United States government. According to the New York Times the total cost of the bailout including commitments for spending, loans and guarantees is $12.2 trillion, mostly in the form of Federal Reserve commitments. To that total we need to add in the cost of the stimulus package of approximately 8/10 of $1 trillion so far.

Add bailout and stimulus, and we get a total for official commitments at this time of approximately 13 trillion dollars.

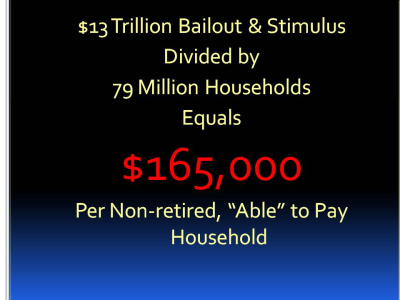

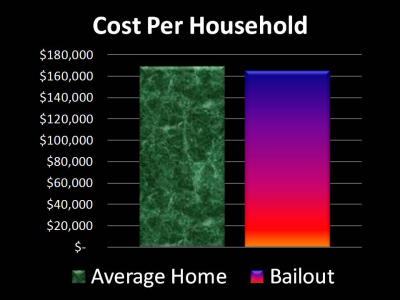

Take the $13 trillion, and divide it by the 79 million households, and we come up with a total of about $165,000 per non-retired, able to pay household. That is a fantastic sum of money and there are good reasons why you never see the government present it in that way, and rarely see the mainstream media do so. That’s almost enough money to buy a house in many states!

In fact, according to the National Association of Realtors, the median sale price of an existing home in the first quarter of 2009 was $169,000. So if we look at the cost to the average household of the bailout package, we could have quite literally bought an average American home with each of our shares of the cost.

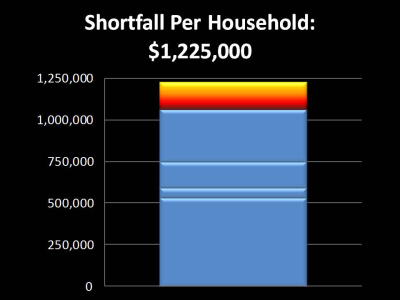

When we add the cost of each of our non-existent new houses to the trouble we were already in, we come up with the sum of $1,225,000 per non-retired, able to pay household.

Your Personal Reality Check

Now here’s my question for you. This is an important question, because the answer could change your standard of living for decades.

At what point did you stop believing that you and your family could pay your share? Was this final $165,000 the straw that broke the camel’s back? The $60,000? The $217,000? Or was it that first half million, the very well accepted half million, that passed your personal ability to pay?

Your answer is vital because once we accept that the average household can’t pay, with not even a remote chance of doing so, then we have to accept that tax increases can’t pay. Meaning these newspaper headlines about taxpayers paying for the bailout are an insult to your intelligence.

So, does this mean the US is bankrupt? No. Long story short, nations that can borrow in their own currency don’t go bankrupt. Not when they can create trillions of dollars out of thin air at will, Shazaam!, much like the Federal Reserve has been doing ever since the crisis hit.

Covering The Gap

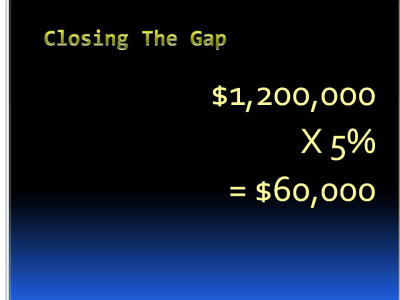

So taxes can’t pay, it’s ludicrous to think they can, and the US doesn’t declare bankruptcy, just how do we cover the gap?

Again, very short version. Pay in full, but make the dollar worth five cents. Drops the per household cost for everything from $1.2 million down to about $60,000. Painful, but manageable over a period of 20-30 years.

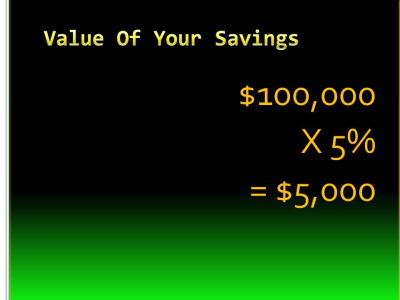

The problem is that this solution also drops your savings to a value of 5 cents on the dollar. Meaning that the $100,000 in savings you have just became effectively worth $5,000. To cover your entire retirement.

History & Solutions

Historically, a collapse in the value of a currency necessarily forces a major redistribution of wealth, and the segment of the population that is most devastated by this seems to always be the same. It’s the retirees, and the people close to retirement. When we look to Germany, when we look to Argentina, when we look to Russia – it is the pensioners who are impoverished more than any other group.

Unfortunately, history is repeating itself again. When we look at the headlines about the destruction of retiree investment values, pension assets and so forth, we're really just seeing the beginning. Because the crisis "solution" that is being chosen, which is creating dollars without the ability to pay for those dollars, essentially represents the annihilation of most of the retirement dreams of the baby boom generation, even if that is not yet recognized. There is not an even cost that is being born by society as a whole, rather some segments are bearing much more of the burden than others. If your peer group (particularly Boomers and older) is headed for disproportionate financial devastation, then happenstance is unlikely to offer a personal way out. Instead, you must instead take quite deliberate actions to change your personal financial position so that wealth is redistributed to you, rather than away from you.

To get out of step with your generation, and have wealth redistributed to you even as your peer group is being devastated by this extraordinary destruction of wealth, you need to start with an essential and irreplaceable step: education. You need to gain the knowledge you will need to turn adversity into opportunity. This will mean looking inflation straight in the eye and saying: “Inflation, you are likely to play a big role in my personal future, and instead of ignoring you or thoughtlessly flailing away at you – I will study you and your ways. I will learn the deeply unfair ways in which you redistribute wealth, and the counterintuitive lessons about how some investors will be destroyed by inflation and repeatedly pay taxes for the privilege, even while other investors are claiming real wealth on a tax-free basis. I will learn to position myself so that you redistribute wealth to me, and the worse the financial devastation you wreak – the more my personal real net worth grows.”

![]()