Chapter Six: Boxing Inflation & Inflation Taxes

By Daniel R. Amerman, CFA

TweetTonight’s feature is a three part boxing exhibition, where Inflation will take on three investors in a row. His first opponent will be the honorable and fair-haired Peter following a dollar-denominated investment strategy. Inflation’s second opponent will be Jack, aka “the Rock”, an all-tangible asset investor known for his steady strength. The final match of the night will feature a title bout between Inflation and his tricky nemesis, Scott, aka “the Pickpocket”.

We'll take a look at the boxing matches from another perspective as well, that of the "House", that sets up the matches and established the rules. The House in this case is the federal government, which both sponsors Inflation and controls the tax rules - how much of each match goes to the government. People may talk about how the House always wins, but few realize just how much the odds are stacked in favor of the House when it comes to boxing with Inflation.

This chapter is part of a book that is in the process of being written. Some key chapters and an overview of the book are linked here.

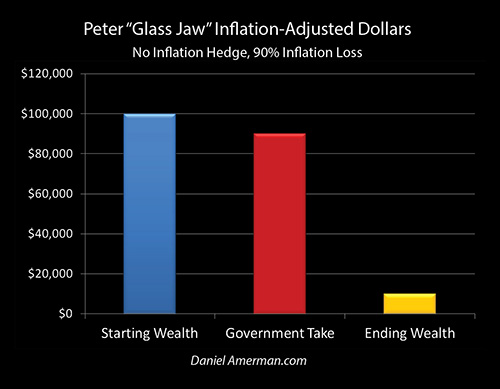

Peter's Dollar Assets

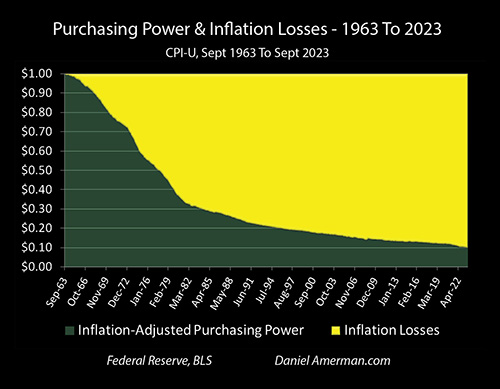

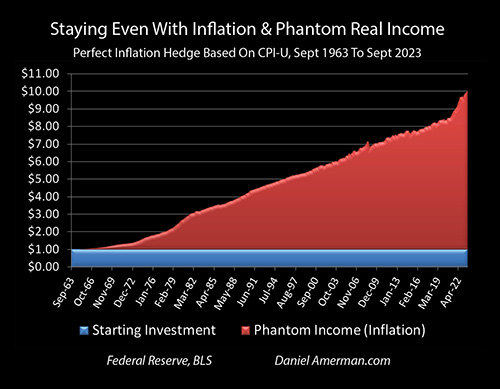

Our starting assumption for all three boxing matches is that 90% of the value of the dollar is lost to inflation. One way of looking at this is what we saw in Chapter Four: this is the historical record of what actually happened to every U.S. dollar in the nation in a single investor lifetime, the sixty years between September 1963 and September 2023. Someone saved a dollar at age 25, and they spent the dollar at age 85.

As explored in that chapter, the Consumer Price Index was 30.7 in September of 1963, and it was 307.8 in September of 2023. That means that it took almost exactly ten times the number of dollars to pay for an average urban standard of living in 2023. The other way of looking at it is that because it took ten times the dollars to pay for an average urban standard of living, that means that each dollar only had 10% of the purchasing power in 2023 compared to what it had in 1963. So, our starting example of a 90% loss in purchasing power is not a wild exaggeration, but simply what history shows us happened in a single investing lifetime.

Another way of looking at this is the future. The United States has an extraordinarily high national debt, and keeping the economy going is absolutely dependent on running massive deficits every year. Economic history shows us the destination, there is no doubt on that account, the only question is the timing. All else being equal - the higher the debt, the higher the degree of inflation. So, it would be reasonable to expect that the next 90% reduction in the value of the dollar will take place much faster than the sixty years it took the last time around. Whether it will take thirty years, twenty years - or five years - is what we will be finding out.

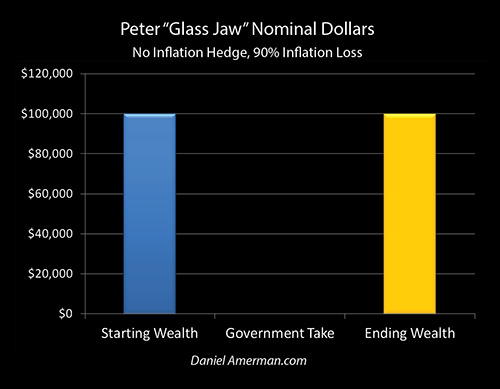

Peter invested for safety reasons to maintain the number of dollars that he had saved - and he was entirely successful at this. Peter started with $100,000. Peter ended with $100,000. Because Peter did not have any income - he did not pay any taxes. The "Government Take" column is therefore empty in the graphic above.

There are a number of different ways that Peter could have done this. He could have kept the money in cash. He could have kept the money in a bank account that did not pay interest - as has been true for so many bank accounts over the last fifteen years. He could have kept the money in a market money fund during a time of government-enforced zero percent interest rates. However he did it, Peter did a very successful job of keeping the dollars that he had already earned - which is the goal of savings for many people.

Jack's Right Jab

Jack was very conscious of inflation - and he was also a strong believer in not getting into debt. Jack purchased tangible assets that kept up with the rate of inflation - land and precious metals. Jack used a steady right jab to keep inflation at bay. Every time the cost of living went up - so did the value of Jack's assets.

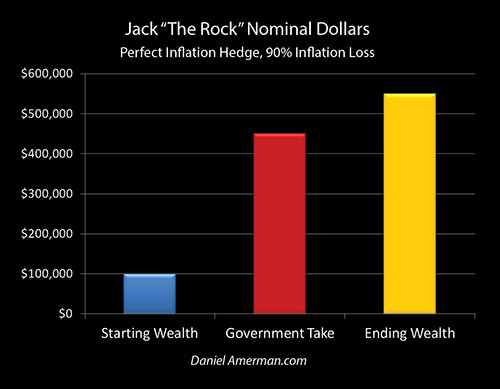

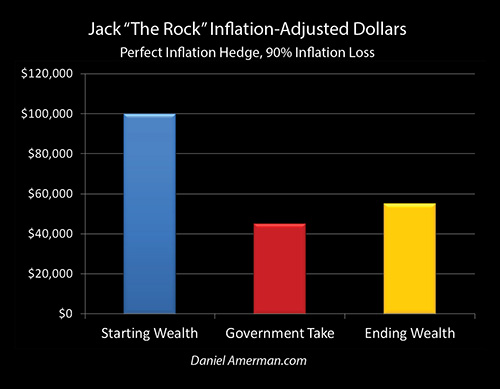

When the value of the dollar fell to ten cents, as covered in Chapter Five, the act of staying even with inflation meant that the value of Jack's assets had to increase by ten times - if his inflation hedge was to be successful. Jack was a highly successful investor, and he created a perfect inflation hedge - his starting $100,000 in investments became worth $1,000,000. A ten times increase in the dollar value exactly offset each dollar buying only one tenth of what it previously had.

However, most people don't view the world in terms of inflation. Instead, they see $100,000 becoming $1,000,000, for a huge $900,000 profit.

While the government created the inflation, the Internal Revenue Service did not recognize inflation as a loss. Therefore the IRS looked at Jack's $900,000 gain and demanded a 50% share of his hugely successful investment profits. The government took $450,000 as shown in the red column above, leaving Jack with $550,000.

Scott's Left Hook

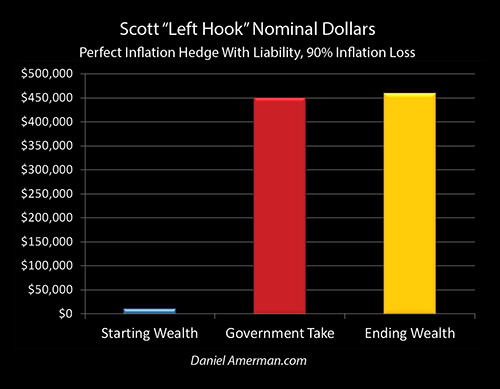

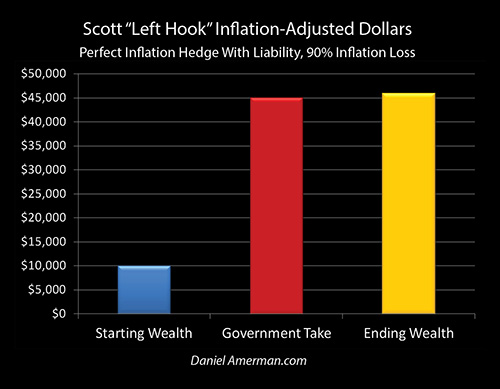

Scott began with much less in savings than Peter or Jack, he only had $10,000. Scott understood how the government used inflation and debt to redistribute wealth to itself, and anticipated that there would be a lot of inflation. So Jack borrowed $90,000 and used the extra money to buy a $100,000 inflation hedge. It was an identical investment to what Jack bought - land and precious metals - and Scott had identical investment results.

The dollar fell to a value of ten cents, and the value of the inflation hedge that Scott purchased increased to $1 million. This was a $900,000 profit as far as the IRS was concerned, so they took $450,000 in taxes, and Scott was left with $550,000 in assets, the same as Jack. Scott, however, owed the $90,000 debt, and after paying that off, he was left with $460,000 in assets. Scott had used inflation and debt in combination to increase his assets from $10,000 to $460,000.

(This is an illustration using round numbers, to get to the essence of the three strategies. In practice, there is an interest cost to the debt, that is being left out for now but that we will be returning to in later chapters. Indeed, the relationship between inflation and interest rates is at the very heart of how the government redistributes wealth to itself via Financial Repression.)

Adding Inflation & Inflation Taxes

All three of our boxers faced an opponent - inflation. To see how the bouts worked out, we need to fully incorporate inflation into the results. We then need to also track the flow of wealth from the boxer to the House, the government. It is only then, that we will see the results in after-inflation and after-tax terms. In the end, these are the only numbers that matter, our remaining purchasing power after taxes have been paid.

Peter invested without regard to inflation. Using our boxing simile, this is like standing in the ring with your eyes shut, leaning forward a bit, with your jaw extended and hands down by your side. Because you don’t realize that you have an opponent. One punch from Inflation was all that it took, and Peter was down for the count. The worst of the damage was done before Peter even realized he was in a fight.

Peter started with $100,000. Peter ended with the same $100,000 - but the dollars were only worth ten cents each. In terms of what matters, purchasing power, Peter lost 90% of what he started with, and ended with only $10,000 in purchasing power.

This was not just a loss of wealth, but a transfer of wealth, as shown with the red column, and as explored in detail in Chapter One. This could be viewed as an economy-wide indirect redistribution of wealth, with Peter's loss being one part of all lenders losing purchasing power, and the government's gain being one part of all borrowers gaining purchasing power (on the principal parts of the debt in each case).

However, there is a good chance that if Peter was a particularly safe and careful investor - as he was - the transfer may have been reasonably direct. If Peter had owned mutual or bond ETFs that were invested in government securities, then his loss would have quite literally been the government's gain. If Peter had held cash, then the cash notes are legally an obligation of the Federal Reserve, and the Fed generally uses the proceeds from that borrowing to finance the national debt. Similarly, if Peter had kept the money deposited at a bank, two of the largest uses of bank money are to finance the national debt, or to finance the Fed via bank reserves, which are then also used to finance the national debt.

That so many of the "safe", easy, and highly encouraged ways of saving money lead to a near inevitable destruction of purchasing power to the direct financial benefit of the Federal government is neither happenstance nor coincidence.

Peter could have tried to get back up and preserve more of what was left of his assets – but even flat on his back, he didn’t understand he was in a boxing match. He thought he was a victim of the economy. He was encouraged in this belief because there were so many tens of millions of people like Peter, that inflation had knocked flat on their backs. So, he just stayed on his back until his $100,000 was only worth $10,000, and 90% of his real wealth was gone.

Peter is most of us, and an inflation “Glass Jaw” where the value of our savings is systematically redistributed to the government is the norm. It is also very important to keep in mind that while what is presented is a round number example - it is also history. The dollar did lose 90% of its value over one investing lifetime, and that loss of value worked directly to the benefit of the federal government. So, this isn't some wild theory. It's what happened before, and it will happen again - the only question being the speed.

The Right Jab After Inflation Taxes

While Peter had no inflation protection, Jack had a perfect inflation hedge. As developed above, and as experienced by the nation for real during the 1963 to 2023 period, the only way to exactly keep up with each 1963 dollar becoming worth ten cents, was to have each 1963 dollar become ten 2023 dollars. As conceptually explored in Chapter Two, and historically explored in Chapter Five, this means that the only way to keep up was to generate nine dollars in taxable income for every starting one dollar in savings.

Jack began with $100,000. As far as the IRS was concerned, Jack generated $900,000 in investment income with his perfect inflation hedge. With a round number assumed 50% tax rate, that meant that Jack had to pay $450,000 in taxes, leaving Jack with $550,000 after-tax. The next step is to take inflation into account, and as each dollar was only worth ten cents compared to the value when Jack invested, that means that the remaining value of his investment was down to $55,000. What matters is what we have after-tax and after-inflation, and the ending bottom line for what is spendable for Jack is that he lost 45% of his beginning assets.

Jack was almost as blind as Peter was. He saw the government coming after him with its right fist, that of inflation - and he was very successful in his defense. “Defense” is the key word here, because that is all Jack was able to do. That may seem an odd statement to many people, as Jack started with assets worth $100,000, and by the time the boxing match was over – his asset was worth $1,000,000.

However, when we adjust for the purchasing power of what that $1,000,000 will buy, our profit disappears. Jack can only cash out for the same amount of goods and services that he had when he started. This makes sense – the whole idea of the tangible asset was to preserve wealth independent of the value of the dollar, and the investment performed exactly as planned.

Jack was, however, blind to the left fist, that of taxes on inflation. Just as Jack was closing out his successful strategy, the government left hook came out of nowhere, and took out almost half of his net worth, leaving Jack flat on his back from the knockout blow. In planning and executing what ended up being a highly successful defensive inflation hedge, Jack nonetheless got blindsided by the tax implications of his strategy.

A Two-Fisted Defense

Scott was the only fighter to see the government using both hands, the right hand of inflation and the left hand of inflation taxes. Because Scott knew what the government was doing, he knew that he couldn't fight the government on a one-handed basis. The fight was rigged if he did what he was supposed to do, as the government created the ring as well the rules for the boxing matches each of us must fight if we are to come out ahead after both inflation and inflation taxes.

Scott exploited those same rules by using a two-fisted strategy against the government. Inflation came straight after Scott as well, but couldn’t close – because Scott had a powerful right jab going. His right jab was in fact identical to the right jab of David. He purchased $100,000 in tangible assets, as the dollar became worth ten cents they became worth $1,000,000 in the act of exactly keeping up with inflation.

However, with his left hand, Scott used the government's own strategy against itself. Scott knew what Peter did not, which was that the government would on a highly, highly reliable basis with the passage of time, wipe out most of the value of its own debts. Instead of trying to fight the extraordinary power of the government - Scott aligned his own financial interests with the government.

Scott financed most of his purchase of the tangible assets by taking out a debt, where the value of the debt would be slashed as the government slashed the value of its own debts. The value of Scott's debt was slashed by 90%, as he aligned himself to benefit from the same exponentially compounded inflation that was reducing the real value of the national debt by 90%.

Scott did, of course, have to pay $450,000 in taxes and he also had to repay his $90,000 debt. $1 million less $540,000 is $460,000, and with a dollar being worth ten cents, that meant that his after-tax and after-inflation net worth rose from $10,000 to $46,000.

In combination, Scott was the only fighter to beat the government's powerful 1-2 combination of inflation and taxes on inflation. And the only way he could do it was to use his own 1-2 combination in response: an asset that kept up with inflation, that was financed by a debt that was destroyed by inflation.

Scott’s net worth was equal to the difference between the value of his assets, and the value of his liabilities. The real value of his assets was staying even, thanks to his tangible asset right jab. The real value of Scott’s debt was plunging with inflation. The harder Inflation came at him – the faster the value of the debt dropped, and the faster that Scott’s real net worth was increasing.

Tracking The Redistribution Of Wealth

Most people think of inflation as being a destruction of wealth, and for most people, most of the time, that is what it is. The purchasing power of our savings is steadily destroyed. The purchasing power of our income - unless it is increased at the same rate as the real rate of inflation - is steadily destroyed.

What is not understood by the average person is that inflation is a quite deliberate and massive redistribution of wealth. Inflation destroys the value of debts so that wealth is redistributed from lenders and savers to borrowers, as we saw above with Peter and in Chapters One and Four. Taxes on inflation simultaneously redistribute wealth from taxpayers to governments.

Those are two massive redistributions, and to see what is really happening, we need to add up all of the boxing matches.

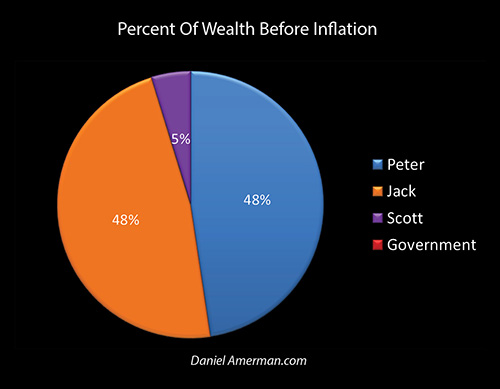

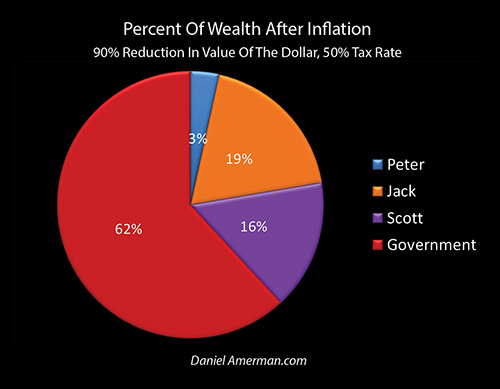

Peter and Jack each started with $100,000 in net worth, while Scott started with $10,000, for a total of $210,000. This means that Peter and Jack each started with about 47.5% shares of the aggregate net worth, while Scott started with about 5%. The government started with a 0% share, and these relationships can be seen in the graph below.

After the 90% reduction in the value of the dollar - which is what historically happened in the single investor lifetime of 1963 to 2023 - Peter had lost 90% of his initial net worth, $90,000, that passed to the government in the form of a $90,000 reduction in the real value of the national debt.

Jack was the target of a much more straightforward taking by the government. In order to keep up with the government destroying 90% of the value of the dollar via inflation, he had to turn $100,000 into $1 million, which he did. After paying taxes on that "gain", he was left with $55,000 in after-tax purchasing power, and the government had $45,000 of his original $100,000 on an inflation-adjusted basis.

Using his 1-2 asset/debt combination, Scott was able to turn $10,000 into an inflation-adjusted $46,000, but he also had to pay the government an inflation-adjusted $45,000 in taxes.

In total then, our three boxers ended up with $111,000 ($10,000 + $55,000 + $46,000). On the other side of the three matches, the government ended up with $180,000 ($90,000 + $45,000 + $45,000). When we add both sides up we get $291,000.

The final outcome of the three boxing matches can be seen in the graphic above. Peter goes from 47.5% of the wealth to 3% ($10,000 / $291,000). Jack drops down to 19% of the wealth, while Scott climbs up to 16%. Most of the wealth, however, goes to the government, as it moves from 0% up to 62% of the after-inflation and after-tax wealth ($180,000 / $291,000).

The House wins, overwhelmingly. The government policies make sure that there will be inflation. The government creates the tax code. And the government is who ends up with most of the wealth.

The Purpose Of A System Is What It Does

There is an applicable concept here that is very important, and that is that "the Purpose of a System is what it does."

There is what people say a System is for. In theory - and this is highly theoretical - the purpose of creating a small annual rate of inflation is to stimulate economic growth. This theory ignores the fact of the extraordinary growth that occurred in the United States for the first century and half of its existence, before modern economics worked out the "secret" of economic growth.

And then there is what a System actually does. If the System "accidentally" creates a massive redistribution of wealth, and that "accident" persists for year after year, decade after decade without ever being fixed - chances are there was no accident, but the redistribution was the purpose of the system in the first place.

The government has created a modern form of money that is historically abnormal. It is not intended to preserve value, it isn't tied to gold, silver or any other asset. It is also not supposed to lose value on too rapid of basis, as happened with the paper money printed in the Revolutionary or Civil Wars.

What this previously unprecedented and unusual monetary system - which is now the norm - does in practice is to produce the historical graph above, which shows the additional dollars needed to stay even, when the dollar was losing 90% of its value in a single investing lifetime. Don't keep up with inflation and lose 90% of the purchasing power of your money even while the value of the national debt is reduced. Or do keep up and pay capital gains taxes - which also didn't used to exist - on the phantom gains.

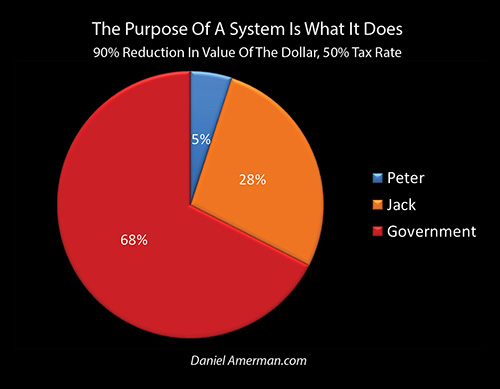

When we put the two new features of our modern monetary and tax system together, we get the graph above. In this case, we've dropped Scott out, and are just looking at Peter and Jack, each of whom start with 50% of the money ($100,000 each), while the government starts with $0.

The ending total wealth is also $200,000, but it has been quite thoroughly redistributed. Peter ends up with a purchasing power of $10,000, or 5%. Jack ends up with a purchasing power of $55,000, or 27.5%. The government benefits from a $90,000 reduction in the inflation-adjusted value of the national debt, even while it collects $45,000 in capital gains taxes on phantom income. In total, the government ends up with $135,000 of the starting $200,000 in wealth, or 67.5%.

With this example - which is restricted to inflation only, with no real income - the government over time uses its two new tools working in combination to slowly take two thirds of the starting wealth of the public, and it does so in a stealthy manner that almost no one understands.

The purpose of a system is what it does.

The massive taking of wealth is not an accidental byproduct. This "novel system" (by long-term historical standards) of using a monetary system that allows for the creation of relentless and reliable inflation over the decades, when combined with capital gains taxes, means that the assets of the citizens eventually become the assets of the government in a highly reliable manner over time.

This applies not just a few people in a few places but to all people in all places. Every dollar saved in 1963 is now worth ten cents. Every taxable asset in every county in every state that kept up with inflation - in the process of doing so generated phantom income that was 9X as great as the original value of the asset.

Keep in mind that this is only the redistribution of value for assets bought with after-tax income. If we include the federal and state income taxes, payroll taxes, and sales taxes collected in the year the money was earned, that the saver had to pay before they had the after-tax savings, then the red area of what goes to the government expands that much more, to likely in excess of 80% for many taxpayers. If there are property taxes that are paid annually on at least part of the investment, and if we take estate taxes into account, then the combined redistribution of income to the government may be in excess of 90% of the pie for some taxpayers over the course of a lifetime.

The other layers are explicit. The dollars are openly taken, and while we are not encouraged to add up the totals of direct income taxes, payroll taxes, sales taxes, and property taxes, we can nonetheless track them in dollar terms. There is another layer of explicit but indirect taxes, and that includes the taxes paid by all the businesses that we buy from, who build their own property, payroll, and other taxes into the prices that we pay.

For a productive citizen, someone who pays into the system rather than receiving distribution payments from it, then as a matter of system design they are going down a gauntlet of sorts where each level takes another piece of what they earned by making an economic contribution. What we have been exploring in these first six chapters is that there are more layers to the gauntlet than most people are aware of.

*****************************************************