Hidden Gold Taxes: The Secret Weapon Of Bankrupt Governments

By Daniel R. Amerman, CFA

TweetWhat if there were a hidden tax that most gold and silver investors were simply unaware of? A tax where the government would take a big chunk of your starting net worth if gold went to $2,000 an ounce, leaving you poorer than you started with? And a tax that rises with inflation, so that $100,000 an ounce gold could cripple your net worth?

This tax already exists, as we will demonstrate in step by step detail using three easy to follow examples. All but a few investors are unaware of this tax and its devastating implications. Simply put, when we assume that gold acts as “real money” and perfectly maintains its purchasing power during rapid inflation, then the higher that the rate of inflation rises, the higher the percentage of the average gold investor’s starting net worth that ends up belonging to the government.

If there is a severe monetary crisis in our future, this could be the most dangerous time in our lifetimes to be uninformed. Investors who are unaware of this profoundly unfair tax, or who choose to ignore it, necessarily become helpless victims of the government.

Knowledge is power, however. When investors become aware of perhaps the number one danger to long term precious metals investment, and adapt their strategies to overcome it – then they can unlock the true investment power of gold during times of currency crisis. And turn potential $10,000 or $100,000 an ounce gold prices into the once-in-several-generation wealth creation opportunities that they should be.

$2,000 An Ounce Gold

In the first step of our illustration, we will consider a situation and how it affects the life savings of two investors. The situation is that 50% of the value of the dollar gets destroyed by inflation. This is not a radical assumption, as with modern symbolic or fiat currencies the value of money is always destroyed by inflation. The only question is one of speed, and if we look at the United States, 80% of the value of the dollar was destroyed by inflation between 1972 and 2007 as measured by official government statistics. For this illustration we will assume there is a smaller loss in value of the dollar, but that it happens much faster – because the US is in much worse shape right now than it was in 1972 in some key ways.

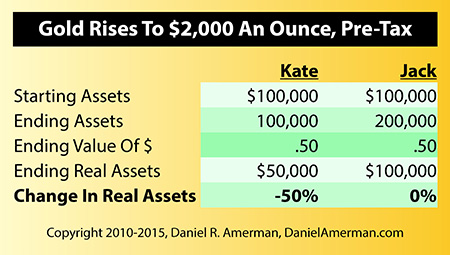

Kate is well educated, keeps up with the newspapers, and is concerned about the possibilities of another round of global financial crisis. So she liquidates her riskier investments, and to play it “safe”, moves her money into a $100,000 money market account.

For our illustration we will assume Kate's money is safe – but the value of her money is not protected. Inflation destroys 50% of the value of the dollar. Kate still has her full $100,000, but it will now only buy what $50,000 used to. Kate has lost 50% of the value of her investments to inflation (for simplicity, we’re leaving out assumptions on interim money market interest payments).

Jack also reads the mainstream media, but reads more widely as well, and believes that high inflation is the eventual logical outcome of the financial situation. Jack therefore takes his $100,000 and buys 100 ounces of gold at $1,000 an ounce (which of course is not the current price, but the numbers in this tutorial are easier to follow with a round number $1,000-an-ounce assumption).

We will assume that gold performs exactly like many investors hope it will. That is, it acts like “real” money and maintains its purchasing power in inflation-adjusted terms. Now, if the dollar is only worth half of what it used to be, and gold does maintain its purchasing power, there is only one way for gold to do so, and that is for gold to sell for twice the number of dollars per ounce than it did before.

Therefore, gold goes from $1,000 an ounce to $2,000 an ounce. Since those dollars are only worth fifty cents due to inflation, we multiply $2,000 times 50%, and we end up with $1,000. Thus Jack's 100 ounces of gold at $2,000 each will buy exactly the same amount of real consumption, of real goods and services, as gold used to buy for him at $1,000 an ounce. Some would say that this is an example of a perfectly successful inflation hedge, where gold has performed exactly like it is supposed to.

The powerful advantages of having your money in an inflation hedge when entering a period of substantial inflation can be seen in the chart below, which compares what happened with Jack and Kate.

Adding Taxes

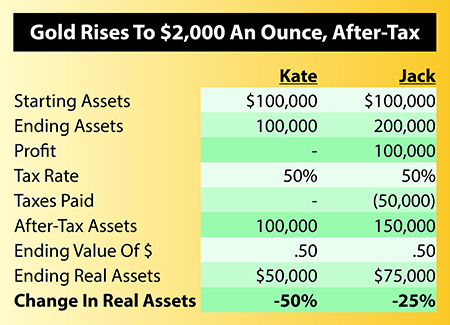

Through placing her money in what is conventionally considered one of the safest possible investments, during a time of high inflation, Kate has lost 50% of her net worth. This is terrible, of course, but at least she should be able to get a nice tax deduction out of this $50,000 loss. Except that when it comes time to fill in her tax return, she starts with $100,000 in her money market fund, and ends with $100,000 in principal in her money market fund. As far as the government is concerned – there is no loss to be deducted. Kate still has every dollar she started with.

Jack decides to lock in his gains by selling his gold investment, redeploy most of his newfound wealth into some new investments, and maybe take a little out to reward himself for having made such a brilliant investment. When it comes time for Jack to fill in his tax return, it shows that he bought his gold for $100,000 and he sold it for $200,000, thereby generating a $100,000 profit. Effectively, the government looks at Jack's having dodged the its destruction of the value of the nation's money, and says “Great move Jack, you made a lot of money! Now give us our share.”

Even in bullion form, gold is currently taxed as a “collectible” in the US, with a 28% capital gains tax rate , or almost half again the highest long-term capital gains tax rate (20%) on most investments, and close to double the 15% long-term capital gains tax rate paid by most investors.

However, even this rate is not sufficient to cover government spending, as the federal government continues to run enormous deficits, with a rapidly aging Baby Boom becoming eligible for Social Security and Medicare benefits, even as an increasing number of younger people come to rely on government transfer payments.

So it is reasonable to anticipate potentially much higher taxes in the not-too-distant future, both in the US and other nations. For illustration purposes then, we will assume a 50% future combined capital gains tax rate on gold – which is not unrealistically high from a historical perspective, as rates were even higher in the 1960s.

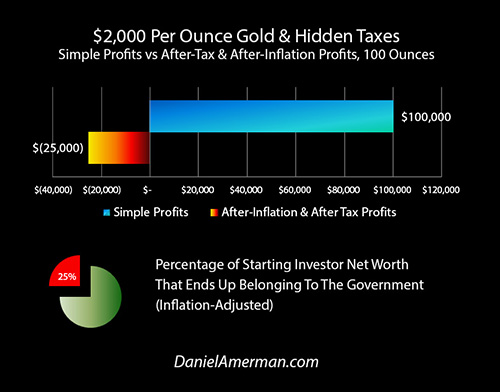

So for Jack, as shown in the chart below, paying a 50% tax rate on $100,000 in profits means $50,000 in required tax payments, and subtracting those taxes leaves Jack with $150,000.

Our final step is to adjust for a dollar being worth 50 cents, so we multiply $150,000 by 50%, and we find that Jack's net worth after-inflation and after-tax has fallen to $75,000. When it comes to what matters, the purchasing power of what our money will buy for us, then Jack didn’t double his money, instead he lost a quarter of what he started with.

Jack just met what are known as “inflation taxes”. And they ran him over.

Turning Gold Into Lead

From a gold investor’s perspective, $2,000 an ounce gold may seem like a dream come true. And when we look at the results of $100,000 turning into $200,000, gold does indeed look like a great investment. Until we remember that the reason gold went to $2,000 an ounce was because of inflation and we adjust our investment results for inflation. We broke even. While not a net improvement relative to today, this outcome is still highly desirable compared to what happened to Kate. Gold did indeed act as “real money”.

Unfortunately, we then run into one of the most deeply unfair and little understood aspects of inflation and investing in anticipation of inflation. Government fiscal policy destroys the value of our dollars. Government tax policy does not recognize what government fiscal policy does, and is blind to inflation. This blindness means that attempts to keep up with inflation generate very real and whopping tax payments on what is, from an economic perspective, imaginary income.

These taxes turn gold from a shimmering dream to a lead weight around our neck, and mean that even a successful inflation hedge can lead to a devastating loss in net worth in after-tax and after-inflation terms.

So how do we deal with this lead weight of inflation taxes around our neck, trying to pull us down under the water? Does all of this mean that we just need to swim harder, to try to overcome taxes?

*************************************************

(The above video is from "Gold Out Of The Box, 2020s Edition", which has quite a bit a more on this and some closely related subjects. Brochure link here.)

*************************************************

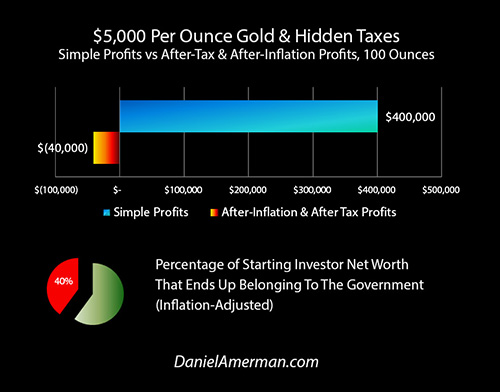

$5,000 An Ounce Gold

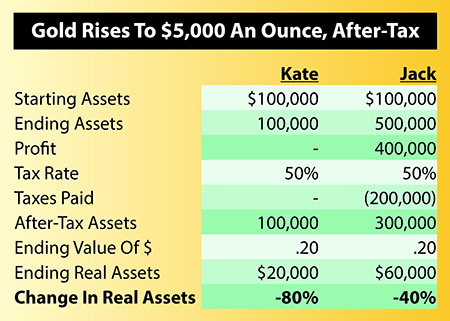

What if gold goes much higher than $2,000 an ounce? What if the dollar falls in value to twenty cents, and we assume that gold again performs as a perfect inflation hedge, and keeps its value? If the dollar drops to 1/5 its value, then the only way gold can keep up is to rise to 5X the dollar price, which means $5,000 an ounce gold.

First let's take a quick look at Kate. She still has $100,000 in her money market account, each of those dollars are now worth twenty cents, and the real value of Kate's “safe” investment is now down to $20,000. Kate has taken an 80% hit to the purchasing power of her net worth.

Meanwhile, Jack has enjoyed some fantastic investment results from his investment acumen. With 100 ounces of gold at $5,000 an ounce, Jack is now half way to being a millionaire!

Jack is ecstatic, at least until he tries to spend some of that half million dollars, and finds out what it will buy for him after he has paid his taxes. Let's repeat our chart from above, but with gold at $5,000 an ounce. When it's time to file his tax return, Jack now has a $400,000 profit to report. Jack therefore has to write the government a check for $200,000 for taxes due, leaving him with $300,000.

When we adjust for a dollar being worth twenty cents, then Jack's real after-inflation and after-tax net worth, what he can buy in today's dollar terms after paying the government, is down to $60,000.

The difference between gold going to $5,000 an ounce, and gold going to $2,000 an ounce, is that Jack loses more of his real net worth. Jack loses 40% of the purchasing power of his net worth at $5,000 an ounce instead of 25%.

The lead weight of inflation taxes is still around Jack's neck, heavier than ever, trying to pull him and his net worth deeper and deeper underwater. Perhaps Jack just isn't working hard enough, and he is going to have to swim like a wild man if he's going to stay afloat, as he will not only have to outpace inflation, but also inflation taxes.

$100,000 An Ounce Gold

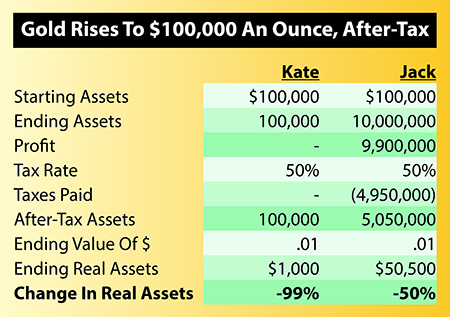

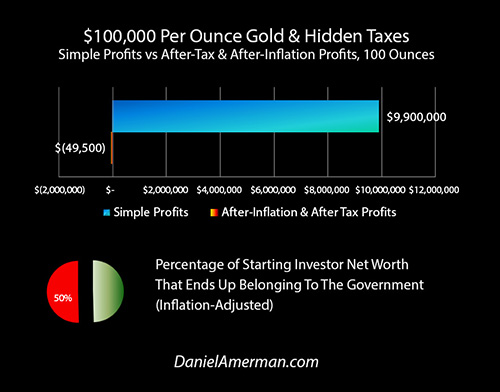

Let's explore what happens if there is hyperinflation and a dollar becomes worth a penny. For Kate, the situation becomes even bleaker as the $100,000 in her money market account will now only buy what $1,000 used to. Kate has lost 99% of her net worth to inflation. Instead of a comfortable nest egg for retirement, she is impoverished, as are the many millions of others who were not prepared for hyperinflation.

If gold (or silver) serves as “real money”, and maintains its purchasing power even as paper money collapses, then to offset a dollar becoming worth 1/100th of what it used to, gold must climb to a dollar value that is 100X greater than what it was. So gold must go to $100,000 an ounce in order to maintain the same purchasing power as $1,000 an ounce gold today. Once again, we're assuming that gold acts as a perfect inflation hedge.

Jack's 100 ounces of gold are now worth a cool $10 million! Jack decides to sell his gold, lock-in his profits, and then start enjoying his new status as one of the ultra-wealthy.

As illustrated above, Jack sells his gold for a whopping $9.9 million profit. The government looks at his profit, and demands its $4,950,000 share. This still leaves Jack a millionaire multiple times over, as he has $5,050,000 in after-tax proceeds. Until we adjust for that technicality of a dollar only being worth a penny. And we find that instead of entering the ranks of the ultra-wealthy, Jack's net worth on an after-tax and after-inflation basis has fallen by almost 50%, from $100,000 to $50,500.

Jack has made one of the most brilliant market timing moves of all time. But the end result is that he loses almost half of his starting net worth in purchasing power terms. What's going on?

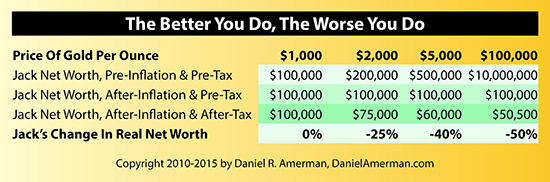

The Better You Do, The Worse You Do

Something seems seriously, seriously wrong here. Jack bets his net worth that inflation will skyrocket, and he buys an inflation hedge in the form of gold. His prediction comes true, a high rate of inflation does occur, and his gold investment does perform as a perfect inflation hedge. Yet the ending bottom-line is that Jack loses a big chunk of the value of his starting net worth. And the better that the gold performs and the more spectacular his returns – the bigger the chunk of his real net worth that Jack loses.

This relationship is summarized in the chart below. When Jack earns a 100% profit – he loses 25% of his net worth. When Jack earns a 400% profit – he loses 40% of his net worth. When Jack earns a 9900% profit – he loses 50% of his net worth.

A Pervasive & Difficult Problem

Inflation taxes are a basic fact of life which investors pay every year when there is inflation. These taxes are entirely real and are deeply painful when we look at the world in terms of what really matters – which is not the dollar amount of our savings, but what our savings will buy for us.

Real as they are, however, inflation taxes are not a line item on our tax returns. There's no box that we check that says go to form “30236 IT” to calculate our inflation taxes. There is no check we write that’s specifically made out to inflation taxes. There's never any discussion in the newspapers or magazines about how much money the average investor pays every year in inflation taxes.

So if almost nobody sees inflation taxes or talks about them – do they exist at all? This may be a good time for a pop quiz of sorts. If you are skeptical, the examples of Jack and Kate were kept very simple for a reason. Go back through the basic illustrations, and try to disprove them. Now, you can change how the price of gold moves relative to the destruction of the dollar, and you can change the tax rate – but there’s no room for anything else.

Do you agree that the numbers work? This “quiz” is self-graded, but your “score” could be essential for your future. Because if our future is one of inflation, then whether and how you deal with inflation taxes may be one of the biggest determinants of your personal standard of living for decades to come.

Also keep in mind that while very high rates of inflation are both a real possibility and made the examples easier to follow - the exact same principles apply with lower rates of inflation. It takes longer to get there, but there is still the same steady taking of wealth from investors by the government through the use of this little understood tax.

Inflation taxes are irrefutable. Whenever you look at investment results on an after-tax and after-inflation basis in an environment of inflation, then inflation taxes make their ugly appearance.

However, while our illustration of Jack and Kate was not all that complicated to follow, the numbers involved are just sophisticated enough where they are rarely acknowledged in conventional personal finance. That combination of just a slight bit of sophistication, with never explicitly appearing on a tax return, means that likely in excess of 99% of the general population is blissfully unaware of inflation taxes.

Let me suggest that a big whopping tax that 99% of voters are blind to represents major opportunity for the government. An opportunity that has been fully taken advantage of by governments, even if the average senator, representative or member of parliament has no better understanding than the general public.

History is bad enough, but as we illustrated with Jack and Kate, the higher the rate of inflation – the worse inflation taxes get. Staying ahead of inflation is hard enough. But even trying to tread water, to stay even with inflation, becomes extremely difficult when you have the lead weight of inflation taxes around your neck, pulling you down. The higher the rate of inflation, the heavier the weight of inflation taxes and the more difficult they are to overcome.

This is true for such traditional inflation hedges as gold and silver. It's also true for real estate. As it is true for stocks. Indeed, almost any traditional inflation hedge has difficulty in reaching the break-even point on an after-inflation and after-tax basis when we take into account the pervasive problem of hidden inflation taxes.

Reversing Inflation Taxes & Creating Wealth

There are two very unfortunate aspects to what we covered in this analysis. Unlike most of their peers, millions of responsible, knowledgeable people are seeing through the soothing, complacent illusions created by the government and Wall Street. They understand the grave threat to the value of their money and their investments. They are moving to the real tangible protection of gold and other precious metals. Unfortunately, in the process, they are setting themselves up for victim status as illustrated herein.

Yes, the “Jacks” of the world are likely to do far, far better than the “Kates”, but despite the dizzying numbers involved with how high gold can go with a truly high rate of inflation – when we look to what our investments will buy for us after we've paid our taxes, our status is still that of a victim.

The other unfortunate aspect is that this simply doesn't have to be. There are two things that gold does spectacularly well during times of financial and monetary crisis. And by using these properties of gold during a monetary crisis of historic proportions, a gold investor can come out of the crisis not just with their net worth intact but possibly even having built wealth on a multigenerational scale.

But let me suggest that achieving this result on an uninformed basis, without fully understanding the issues discussed herein, will be a matter of rather unlikely good fortune.

There is a better path. Study. Learn. Invest in your intellectual capital. As covered in my “Gold Out Of The Box” materials, let gold do what gold does best. Let gold provide safety and security for you. Unleash the wealth-creating abilities of gold during peak inflation to multiply your real wealth. But don't simply rely on gold as an inflation hedge while ignoring inflation taxes.

To have a chance of beating inflation taxes, we not only have to realize they exist, but we need to thoroughly understand our opponent. Our opponent is an enormously powerful government that is deliberately blind to the effects of inflation. Government fiscal policy destroys the value of our money. Government tax policy is officially blind to inflation. So a crushing hidden tax is created that keeps us from maintaining the purchasing power of our savings, with our attempts to survive the deadly effects of inflation merely acting to increase government tax revenues.

The key to prospering in a world of inflation taxes is to understand that regardless of its strength, a blind opponent is ultimately a weak opponent. Through careful study and by focusing very closely on the intersection between taxes, net worth and inflation, we can discover how to turn inflation into gains in real wealth, to which the government is entirely blind. We can learn to reverse inflation taxes, so that instead of paying real taxes on imaginary gains, we are paying imaginary taxes on real gains. Entirely legally, with every cent of taxes due paid in full – because remember, inflation taxes don’t appear on your tax return, and neither does their reversal.

********************************************

Watch The 2020s Edition Online

Learn more about the contracyclical strategies for gold and stocks, brochure link here.